The Contents of this page is dealt with in other parts of this site

I have been told by Victoria Police that a document in this site relating to South Australia Police has been downloaded and modified and used by someone in a scam. Such actions would warrant severe criminal penalty from relevant authorities.

1. Evidence of Conspiracy & Cartel:

Globally no competition between lenders in applying the repayments to Principal & Interest in different ways. All apply first fully to interest. Is that not a conspiracy/cartel/ anti competitive arrangement?

CEO knows they are charging compound interest, but his own branch managers in Victoria confirm they are charging simple interest.

1. Commonwealth Bank of Australia Letter Confirming Interest Compounding on loan. He says it is 'industry practice', meaning NO Competition between lenders in relation to compounding monthly, a Section 54 criminal offence under TPA 1974!!! I have not had a loan with CBA and not a customer of CBA but received this in response to letters sent to 14 CEOs as my initial efforts of getting the politicians or media or any of the government departments to do anything in this matter yielded no results.

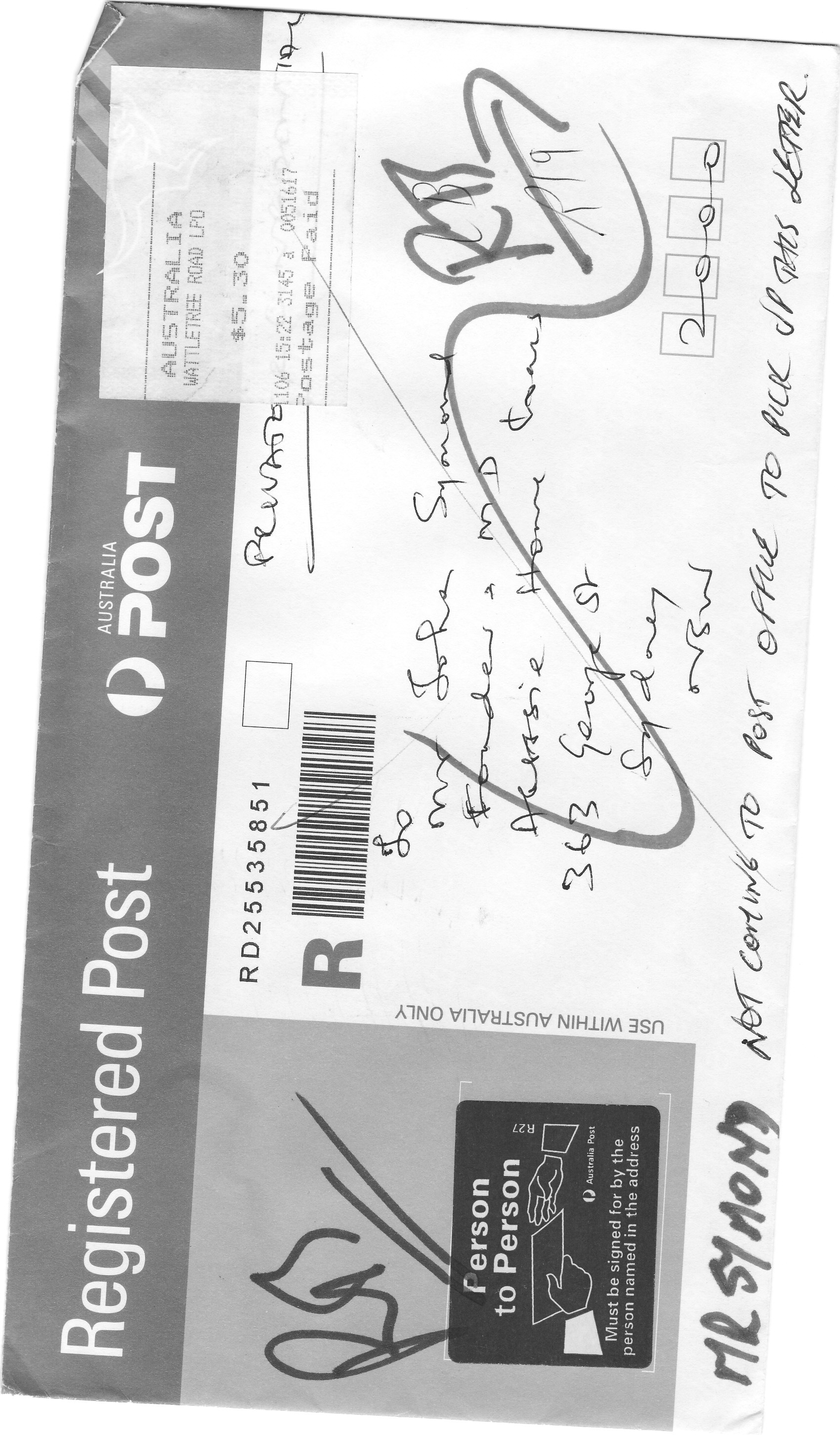

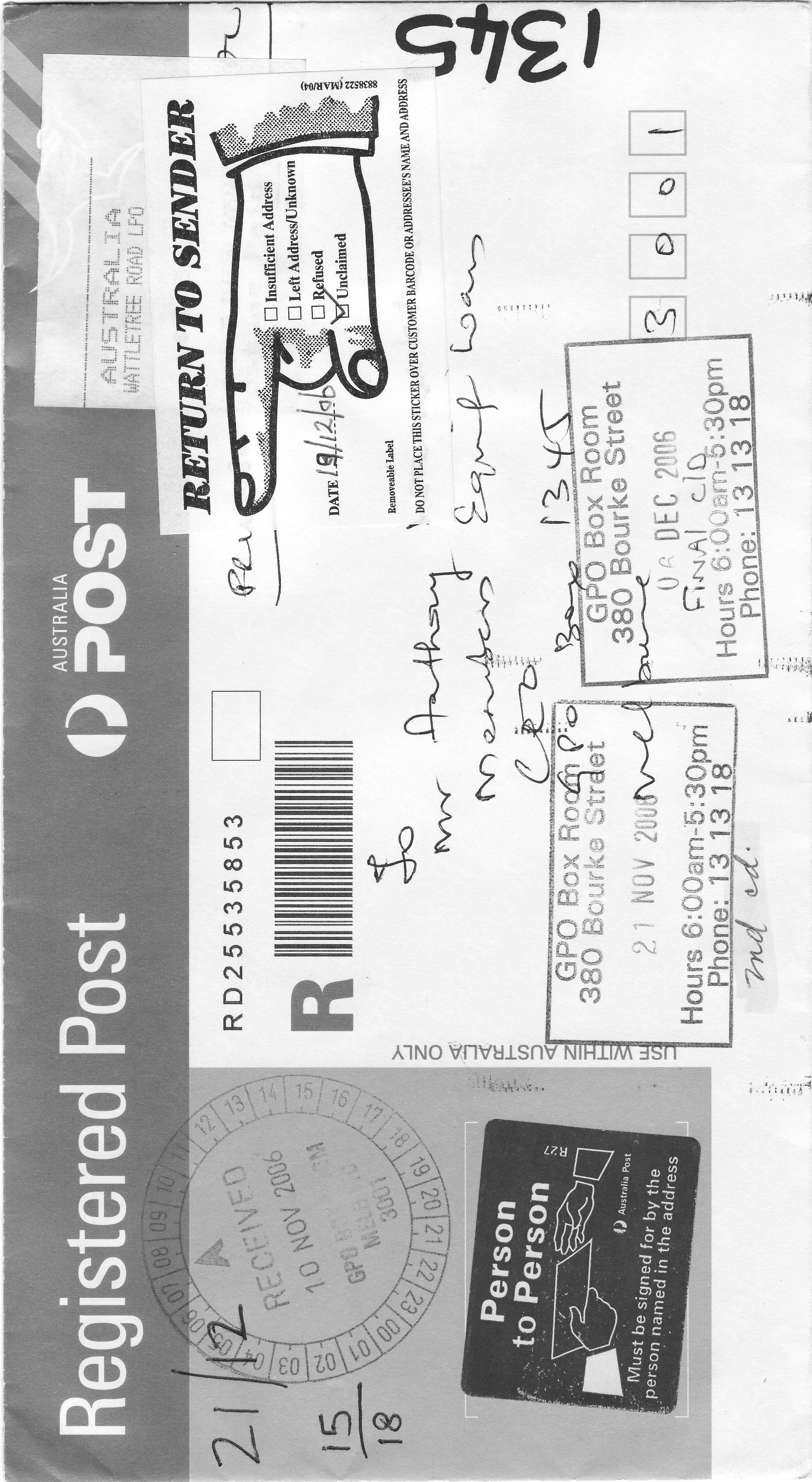

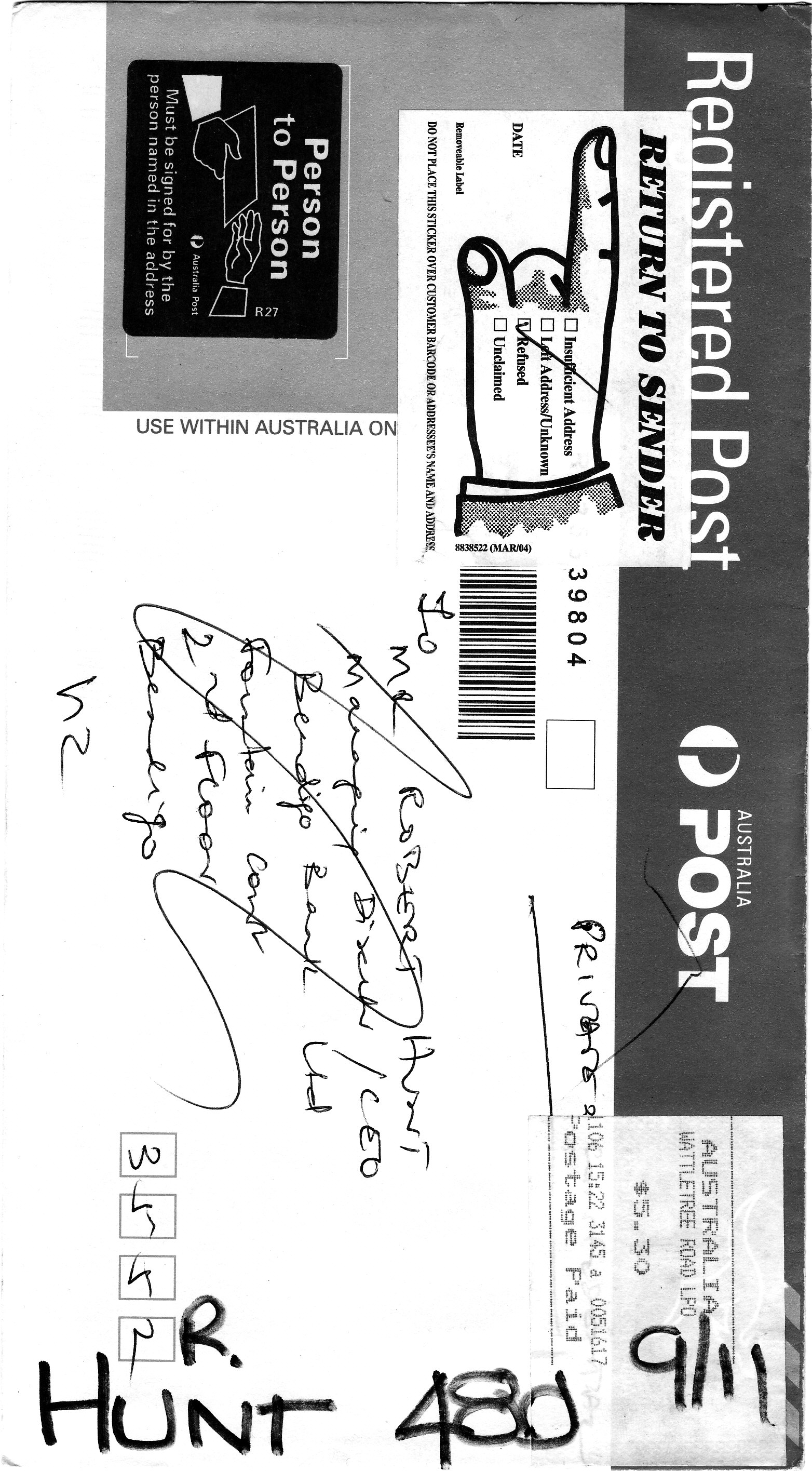

2. Letter suggesting to charge simple interest on loans (so that that bank will get entire market share of lending in Australia), sent to CEOs of 14 major lenders in Australia with 'registered post person to person option' (paying additional postage for this special service). Guess what 4 of the CEO's refused to accept delivery of the registered post and sent back (Aussie home loans, Members Equity, Bendigo bank and National Australia bank, but how did the CEO's knew what was inside registered post? Have they not proved they have close connections and understandings with other CEOs?) and 4 of the remaining 10 sent replies. Refused AussieHL, Refused Members equity, Refused Bendigobank

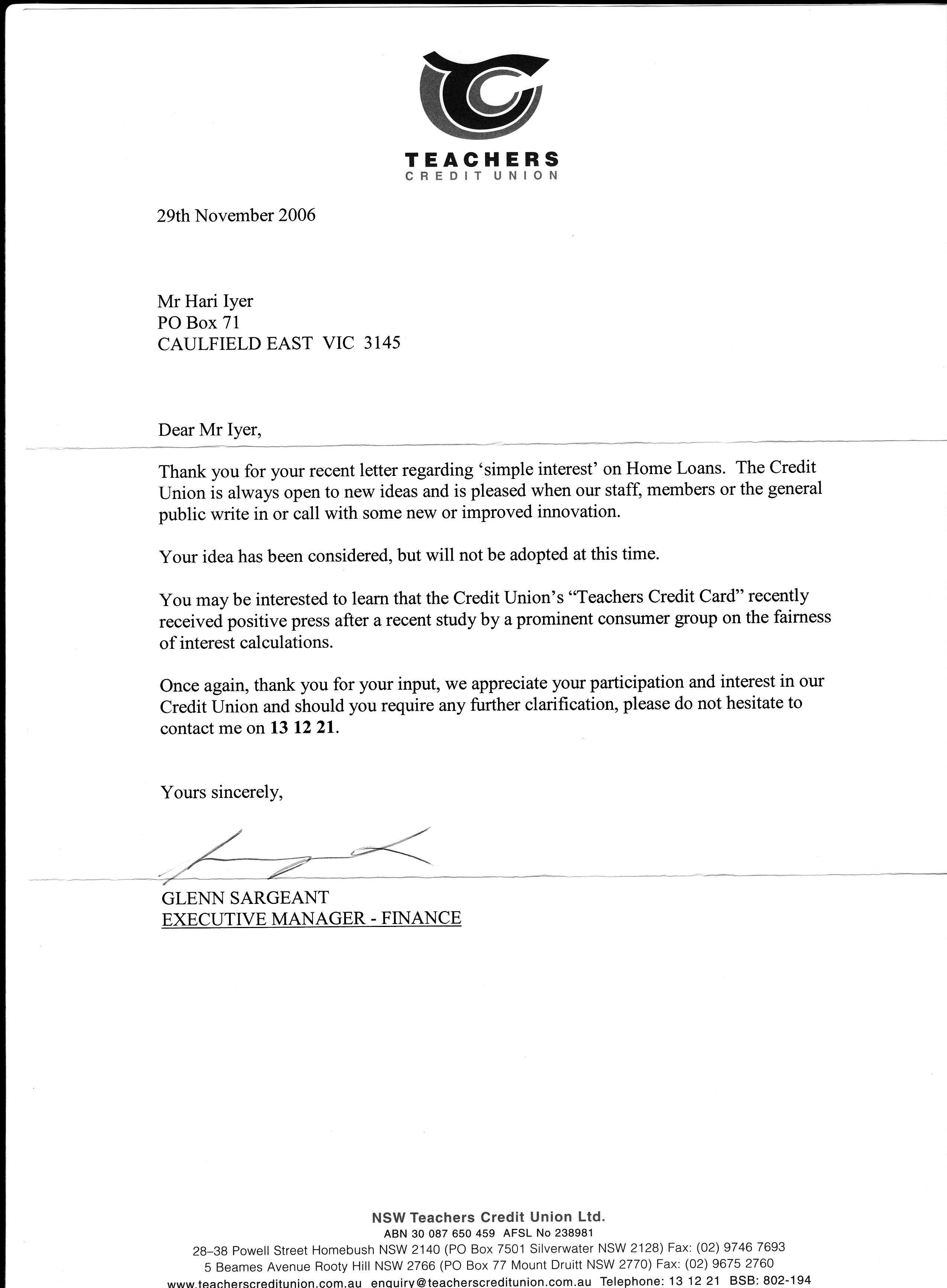

Letter to ANZ, Letter to aussie, Letter to Bendigo, Letter to CBA, Letter to credit Suisse, Letter to hsbc, Letter to Macquarie, Letter to members equity, Letter to Mortgage choice, Letter to NAB, Letter to Rams, Letter to st Georges, Letter to teachers cu, Letter to WBC, Letter to Wizard.

Reply 1 CBA Reply 2 st George Reply 3 anz Reply 4 teachers credit union

2. Westpac Related Documents:

(their managers repeated they charge only simple interest!)

I sent my complaint to Westpac online regarding charging compound interest without disclosing and hence to return me the difference. For this I received a rude call from Robyn Clarke and then she sent the letter below asking me to go to ombudsman. Letter from Robyn Clarke of Westpac, not saying anything about compound interest. Page 1, Page 2.

Ombudsman's reply to my formal complaint Page 1, Page 2. He raised his hands up clearly saying that they are not aware if they have power to deal with this kind of complaint, but will try his luck asking the bank.

Minutes of telephone conversation with Mr Tim Goss (National resolution manager of Westpac) (in relation to complaint with ombudsman) , in 50 minutes of my talk I asked him 5 times if they are charging simple interest or compound interest, he was more of a passive listener (at one point I even thought he went to sleep) and finally he wanted me to make a guess of simple or compound!! Then he wrote a letter repeatedly confirming that they charged ONLY SIMPLE INTEREST on my Loan. Please compare with what is in 1 above!! Page 1, Page 2, Page 3, Page 4. False Misleading and deceptive (conduct?) communication in writing!!! But Justice Harbison did not allow me to go through presenting my case, I was directly put in witness box in spite of telling her that was my debut presence in court. Ombudsman closed the file with Tim's explanation Page 1, Page 2, Page 3.

Westpac's Threat to me to take over my assets if I did not pay the court cost for my second case before 16th April 2008. Page 1, Page 2, Page 3.

3. National Australia Bank related Documents:

(their managers saying they charge only simple interest!)

Email correspondence with Mr Anthony Thompson, (national reconciliation manager of NAB) proves that he was not aware that they charge compound interest on loans

Complaint against National Australia Bank with Ombudsman fixing the time limit for NAB to reply by 18th Dec 06. Page 1, Page 2.

Mr Alejandro Young's reply (no other contact made before or after this letter from NAB, either on phone or written correspondence) dated 19th Dec 2006 (clearly proving the arrogance that Ombudsman cannot do anything. I say arrogance because, Alejandro is a higher level officer than Anthony Thompson to be careless and negligent in complying with ombudsman's instructions. Since Ombudsman system itself is only a 'dispute resolution mechanism' maintained and paid by the Banking industry, how can ombudsman give regulatory instruction? Mr Young's letter Page 1, Page 2.Clearly showing a high handed behaviour threatening not to go further! Ombudsman closed the file by writing to me this letter, Page 1, Page 2, Page 3.

4. Commonwealth Bank of Australia Documents:

(their managers assure 100% they charge simple interest!)

Ms Tommy (lending manager of commonwealth bank of Australia, Cheltenham branch)

Mr Gary Carter (manager of Commonwealth Bank of Australia) assured 100% they are charging simple interest.

Narelle Hosking and Mario Brex (Commonwealth bank of Australia) did not want to say compounding.

Justice Marilyn Harbison the head of Anti discrimination wing of VCAT, proves in her judgement she does not know if that was simple interest or compound interest.

5. Cover Ups by Departments & others:

My letter to ACCC. Followed by Minutes of telephone conversation with ACCC (Australian Consumer & Competition Commission) raising their hands up saying they are NOT responsible for Banks!!! Though I taught Trade Practices Act for 2 year in Victoria, where ACCC is responsible for any supplier of goods and services if they do False, misleading and deceptive conduct or advertisement! Normally, as per their website, they will act on anonymous complaint itself, against offenders, but this time they chose to get in touch with me only after I sent 2 complaints with one month gap (as they didn't do anything on first complaint). ACCC's reply (lifting their hands up, they are not responsible) Page 1, Page 2, after the telephonic conversation. So complained to ASIC.

ASIC's reply. My response (Australian Securities and Investments Commission, a watchdog for companies in Australia).

Emails between Alya, staff of ASIC, and myself. ASIC didn't want to take any available action due to regulatory impact!!!

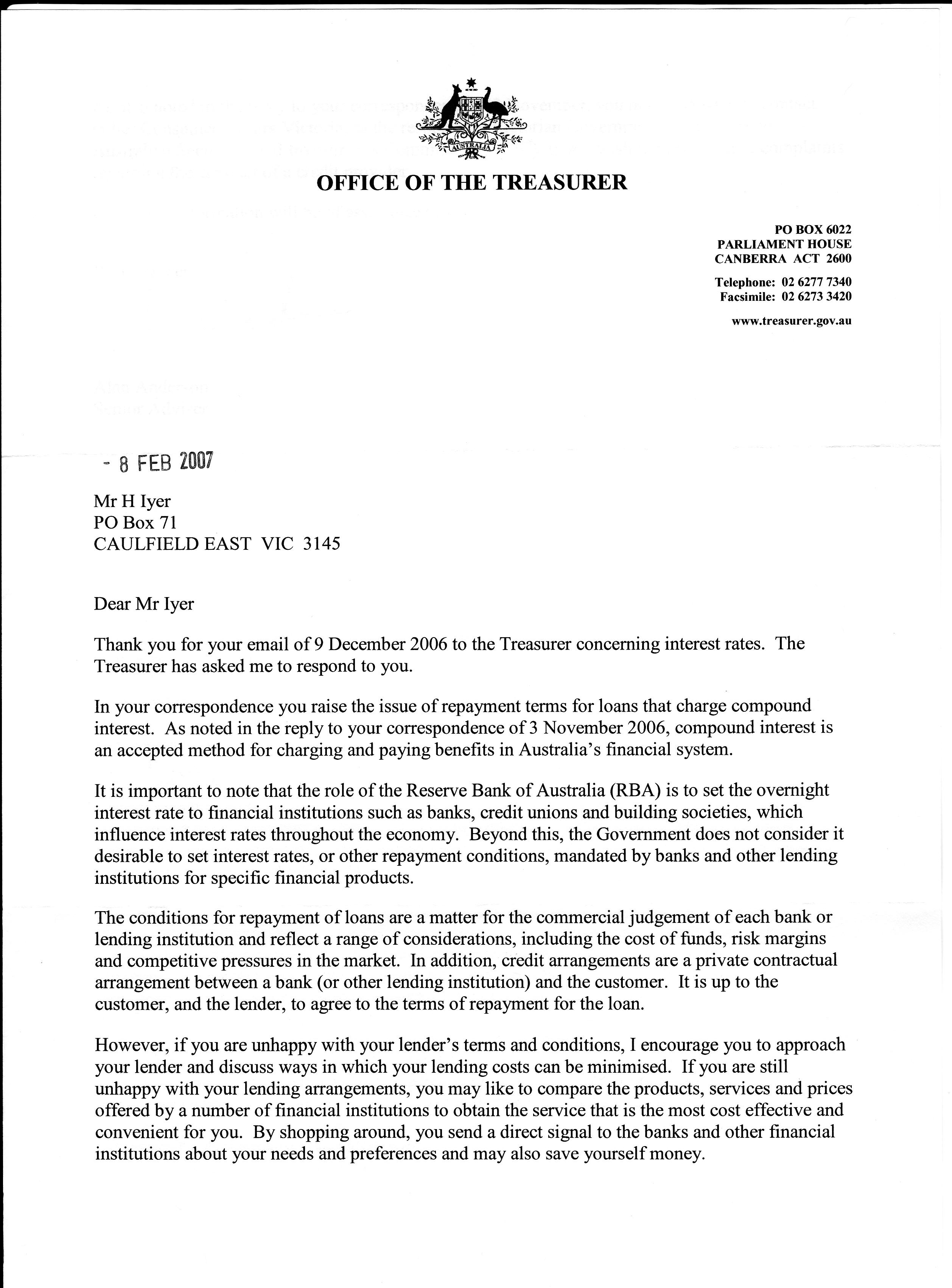

But I already went to Mr Peter Costello, then Treasurer and the then prime minister Mr John Howard and got this below. Response from Special Advisor to Federal Treasurer then Mr Peter Costello, asking me to go back to ASIC. Page 1, Page 2. Either Peter Costello's special advisor is crazy or the ASIC representative has gone crazy, or both together tried to drive me crazy! Another letter from Treasurer Page 1, Page 2.

Prime Minister of Australia Mr Kevin Rudd, carefully helping Australians in his 'attempt' to manage 'grocery prices and petrol prices' has left it to me to manage the bank compound interest issue. Perhaps his department does not know that ASIC has sent the above letter to me already and that Mr Peter Costello's department already sent such replies to me. Why they wont know it? I didn't write a letter to Kevin, i sent email via his website requesting him to look into my website (where i already have these letters in the website), perhaps his department does not know how to go through the website or may be their computer were not functioning properly, but since they wanted to give me 'a reply' wrote me this reply here.

Licensing requirements by APRA for a bank. So went to APRA (Australian Prudential Regulation Authority, a licensing body for banks in Australia), my first email correspondence, they say they are responsible ONLY for Deposit side (have you ever heard of dentist only for bottom row of tooth??) of licensing and NOT lending side!!. Their reply and my gratitude that highlights that my claim regarding compound interest on loans, "raises several issues"

Letter 27 nov 06 to ATO regarding ID 298/2006 where the commissioner, after the Hart V FCT case that went in favour of the tax payer, brought a new terminology of 'FURTHER INTEREST' (to mean interest on interest not to be allowed as tax deduction. Clearly he was aware 'interest on interest' is NOT tax deductible, but what he didn't want to consider in my letter is that ALL lenders in Australia charge compound interest ONLY). ATO's withdrawal 1 dec 06 of ID 298/2006, and letter to ATO regarding revenue loss to Government and losing say $100 as interest expense deduction and related tax offset and taxing the lender at 30% of such income. Letter 13dec06, Letter 02March07, Letter 31 mar 07 (this letter I sent as registered post person to person option but till 7th Aug 07 I didn't receive any acknowledgement from the commissioner, so I wrote the next letter and sent only by ordinary mail), Letter 8 aug 07,(i received a reply for this in 2 days reply from ATO...reply regarding client framing up) Letter 16 aug 07. ATO reply 10 aug 07.

ATO's officials Jason (tried to threaten me for sending letters to commissioner, since it did not work with me), then Paul (tried to persuade not to bother about this interest matter any more, he went in shame when I asked him if he has not been provided with a rubbish bin) then Kathy spoke very highly appreciating my research. I asked her to send a written acknowledgement for whatever I communicated, listing the dates of my letters and basic message of compound interest and 'interest only loan as attracting anti- avoidance provisions of Income Tax Act. She agreed to send one but asked me to stop sending any further letters. So I told her to make 'tax fraud as legal' than telling me to stop sending letters (she laughed) and this is she sent in writing!. Kathy's letter (there is no reference number to track this document down later on as to from where this letter came to me, there is no address as to from which section or branch office of which state this letter is generated from and I could not, could anyone make out that this letter is in response to my complaints about banks charging compound interest and all tax agents claiming compound interest as tax deduction and that the government is losing billions of dollars each year by this, and that 'interest only loan' promoted by banks is satisfying the Part IVA (anti avoidance provisions) of Income Tax Act, that it is a 'scheme' and it is 'solely or predominantly' promoted to avoid paying tax or gain a tax benefit. (you can see that ATO is capable of sending such anonymous letter to me when I reported such a serious tax fraud). ATO's reply on 27 March 07.

Letter from Queensland fraud and Corporate crime group, in response to my complaint of non disclosure of compound interest, the department saying non disclosure is not a crime!!!. Letter from South Australia Police department in response to my complaint about the interest.

Lodged a few written complaints with Sunshine Police station and Malvern Police station that Westpac and National have taken money out of my loan account and that they be charged for fraudulently taking money from me, recover that money and offered my assistance in framing charges and proving in the court. Till date I never received acknowledgement of registering such complaints, but I have the postal acknowledgement for the complaint having been delivered by Australia post! Letter 281106s, Letter to crime stoppers, Letter 04dec06s, Letter 04dec06m, Letter 181206s, Letter 181206m, Letter 020107s, Letter 020107m, Letter 090107s, Letter 090107m, Letter090107s1, Letter 090107m1, Letter 010207s, Letter 010207m, Letter 070307s, Letter 070307m. For all these I sent as registered post (to sunshine station and Malvern station, till date I never received an acknowledgement for having received these complaints and registered them. So the moral of the story is when banks do fraud, NO LAW on this land, but when a child does shop lifting ..... ) (I am not saying shop lifting is right, but the reaction shows for a small crime is quite different compared to the reaction for my loud cry about lenders fraud!).

As part of ‘framing me up’ operation (perhaps the way they would have thought the Judge would be influenced not to allow me to speak in my case against Westpac), a large client of my accounting practice, in collusion with Mr Peter Beatie of ATO (he is a farmer manager of Westpac Bank) caused a courier driver to forge my signature, as if he delivered a parcel of my client documents to me. He used the correct spelling of my name as 'Hari', confessed to me he did sign without my authority on my behalf. I asked him to reveal the person who advised him to do so, which he didn't want to disclose. I told him I would go to court for that. Went to Malvern police station, faxed details of the case. Their reply that no criminal offence. Letter from Police Commissioner, Ms Christine Nixon's office, as I escalated the matter to the commissioner (later confirmed Malvern police decision is correct). Please note Malvern is the constituency of Mr Peter Costello and some prominent senior members of Victorian Parliament too, so it is not that easy to get police support in such environment.

Emails to Governor general, reply1, reply2 & Queen

Sent to Queen Lender's fraud borrowers over 20years or @PMT failure, got Queen's reply

6. Court Case Related Documents:

Against Westpac

1. Full case and arguments submitted against Westpac Banking Corporation to VCAT.

2. Westpac Lawyer's fax on 19 Feb 2007 pleading to meet me prior to hearing scheduled for 22 Feb 2007 (directions hearing)

3. 22 feb 2007, Deputy President Ms B Steele, decided (after her encouragement to me to go for Compulsory Conference, to Compromise with Bank was vehemently refused by me, full transcript of proceedings on 22 Feb 07) full day hearing scheduled for 19th March 2007. My letter to Ms B Steele regarding VCAT powers and for her own benefit in the position she was administering to public, as she was not aware of VCAT's powers to order interlocutory injunction against Westpac. Page 1, Page 2.

4. VCAT altering the decision made on 22 Feb 2007 to allow a full day hearing (from commencing from 10.00 a.m. to commencing from 2.15p.m., court ends by 4.30p.m)

5. Westpac's revised defence letter (as the first defence letter, from Mr Sam Ure, was not worth standing for minutes in the court). They knew on 13th March the Judge who would preside over on 19th March, whereas the judgement and the reasons for her decision is NOT yet made known to public by placing in legal database. Page 1, Page 2, Page 3.

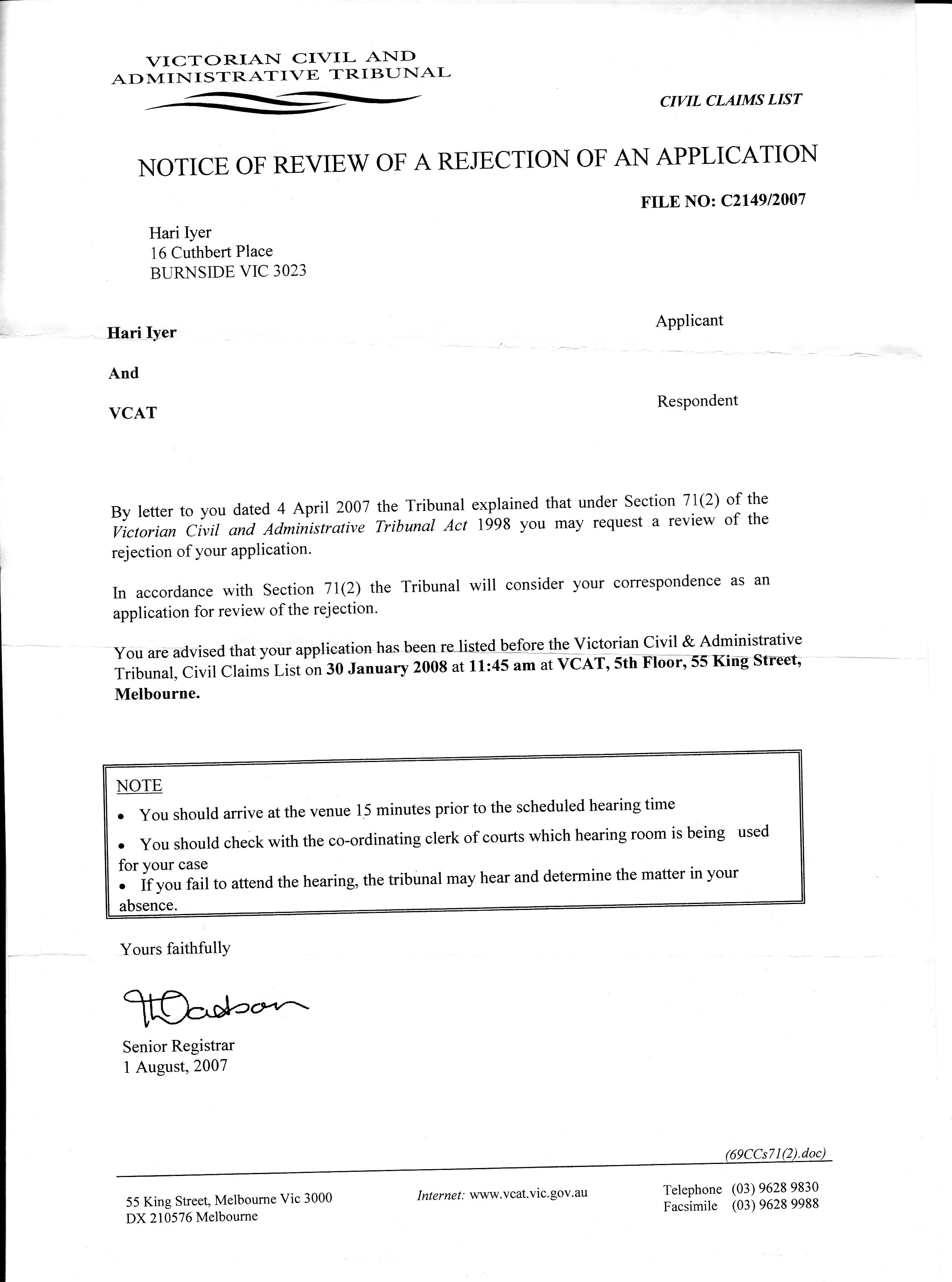

6. Then followed the hearing and dismissal on 20th March 2007, by Justice Harbison and making me pay $ 10,000 to Westpac before 30th April 2007 (shortly I will place the transcription here in couple of weeks). Transcript of 19th March 07 hearing, 20th March 2007 hearing. My new case against Justice Harbison filed on 27th March 2007 and VCAT's response to it, i insisted in registering the case, rescheduling and final withdrawal due to my overseas trip. (shortly i put the email link in withdrawal).

7. Sudden resignation by Chief Judge of VCAT on 21st March 2007 (not only he resigned from VCAT, but also from Supreme Court Judge position, hats off to this person who has a backbone and principle not to budge for anyone's pressure when it came to his role of being a Judge to deliver Judgement, perhaps he has good realisation of who a judge is for the public). Please note my case against Westpac where I was tried in witness box than trying Westpac, was decided by Vice President Judge Harbison and 21st March 07 morning I formally requested for 'transcription of proceedings (to know what happened on 19th and 20 March inside the court).

I felt uncomfortable about my second case against Westpac, in the same court.

Still believed in my philosophy that not all in a place can be bad and i would get justice from the same court.

8. So I applied to Attorney General Rob Hulls, (second one on 22april07) as there existed 'conflict of interest' in my understanding. (www.countycourt.vic.gov.au). Honourable Rob Hulls reply. My letter to John. Then I complained to Legal services commissioner, their reply 1, reply 2, reply3, reply4. ((will attach reply 2 shortly they only confirm that Judge Strong didn't not appear in disguise, but have not confirmed if he is a twin brother with Mr Strong who appeared for Westpac and if he was not related to Judge Strong)

VCAT has (you can visit VCAT website www.vcat.vic.gov.au) President/Chief Judge who is a Supreme Court Judge, below this position two vice presidents heading two wings of VCAT. Anti discrimination wing headed by Justice Harbison and Civil list wing by Justice Bowman. Besides the two judges at VCAT at 55 King Street, Melboune 3001, there are 5 other Judges & 'Vice Presidents' presiding over at county courts.

One of the Vice presidents is "Judge Strong". He is supposed to be at, Melbourne County Court, 250 William street, Melbourne 3001. It is just the next street and about couple of blocks away from VCAT building. He was heading Work cover 134AB lists. Perhaps he may have been a senior to Justice Harbison at VCAT. From the transcripts (attached link above) on 10th May 07 one can notice clearly the way Mr Strong was 'brain jacking/hijacking'. If he was only a counsel for Westpac, Senior Member Vassie did not have to take up his 'dictations/directions as gospel.

So I searched (because the way Justice Harbison regarded and took the directions of the proceedings from Mr Strong, on 19th March 2007, I realised he must be some important character) and identified Justice Strong as vice president of VCAT. I sent email to Andrew Anchan. He searched and brought an annual report with the photograph and we both found that the picture is of the same person who appeared for Westpac.

I wanted to reconfirm this in person, face to face. I searched his location in Melbourne county court. Went to attend his session on 2nd April 2007. That day the court announce about 10a.m that he won't attend due to ill health. Next he was scheduled for 'sentencing' on 4th April 2007 in Court 7-3 of Melbourne county court at 10.00 am in Di Lalla, Michelina (a lady who was accused of pouring petrol on the head of her husband to set him on fire) and at the same time in the same venue he was scheduled for delivering a Judgement in Mickoski - V - Munroe Livestock pty Ltd & Anor.

I knew for sure he has to be there to deliver the sentencing at least. So I sat in public gallery for him to look at me so that I can be sure if he was the same who attended as 'Counsel for Westpac Mr Strong'. To my surprise he definitely resembled the same. I waited to hear the voice, to recognise if the voice was same, for me it really matched.

Besides, after seeing me there, Judge Strong firstly addressed, a few times, the crown lawyer with wrong name. The bench clerk went close to him and advised the correction. Then the judge announced the correction to all and apologised. So I believed he was the one attended my case or at the least his twin brother or a close relative must be the one who attended for Westpac. So I complained to attorney general and other officials. But now one part is definitely confirmed that Judge Strong is NOT one and the same person as counsel Strong but the second part if he is a twin or the counsel is related to the Judge only God knows.

9. VCAT accommodating Bank's request not to schedule hearing on few dates, but my similar request (that I was not available on 20th March 2007) has been totally disregarded and Justice Harbison, though Mr Strong finished his presentation by 4.10, didn't allow my request not to have hearing on 20th, and scheduled for early morning first case 10.00 am and made it mandatory for me to attend. Please note she is the head of anti - discrimination wing of VCAT.

10. Section 75 application filed on 2nd May 2007 by Westpac on my second case, to include such hearing on the already scheduled 'directions hearing' on 10th May 07. Vcat received their request on 2nd May, Vcat decided & posted on 4th May 2007, a Friday (Saturday and Sunday in Melbourne no postal delivery, so I received on 8th May 2007, Monday, but hearing was on 10th May 2007. It is usual for the court to provide 2 weeks for the respondent, myself, to file an affidavit in relation to section 75 application filed by one party, Westpac) their decision to include Section 75 hearing on 10th May 2007. Page 1, Page 2. Mr Vassie on 29th March 2007, Mr Vassie on 10th May 2007.

7. Court Case Related Documents:

Against National Australia Bank

1. Full case and arguments submitted against NAB, same against CBA

2. Affidavit submitted by NAB for section 75 (requesting the court for summary dismissal of my application to court) Page 1, Page 2, Page 3, Page 4, Page 5, Page 6. My Affidavit submitted against NAB's Section 75 application for summary dismissal against 1 above.

3. You can see the presentation in court on 18th June and 20th June 2007 from the judgement delivered on 23rd January 2008.

4. Letter to Justice Bowman as further submission. For this i received a reply from Mr Bill Swanie from VCAT advising that my case is dismissed and no further communication is entertained.

5. Proving compound interest and that accounting profit is manipulative, both documents proved in the court. Compound interest proof. Accounting results manipulative.

8. Other related documents:

1 Federal Senator Fielding enquiry on 'Bank Fees & Charges" (not about method of charging interest on loans!!!).

2 Criminal Codes Act 1995 relevant Part 7.3 and 7.4 pages 236-249 shows criminal offence committed by these banks! Case citations and basic Trade Practices Act and its difference with other legislations.

3 Consumer Credit Code web download regarding Mandatory Comparison Rate Act 2003 requiring the lenders to disclose as a "single percentage per annum" the "total cost" of the loan. Either the Act is NOT speaking proper English (which I believe is speaking clearly) or the Banks and lenders are from Non-English speaking background!!! (perhaps only way to escape).

4. Special Characters. Shaun & James, Praveen Rao, Andrew, Peanut allergy, Praveen's tax email.

5. Highest income tax paid ($3 million) by a client of the practice who operated airline service for ADF (Australian Defence Force) to transport people and supplies to Afghanistan, Iraq etc. Page 1, Page 2.

6. Westpac bank statement where $1.2million has come in and gone out in Jan - March 07 to a client of my practice who made his attempt to back stab. Page 1, Page 2, Page 3, Page 4.

9. Publications of books on this:

1. Lender's fraud borrowers over 20years or @PMT failure a book of 28 pages explains in common person's language why compounding interest is NOT appropriate, at least on long term loans.

2. Covering? an 'Un coverable' a real experience in Melbourne, as if I have been corresponding with 'clowns' heading various departments.

3. Business Plan and Cash flow & Profit and Loss budget I prepared, for starting a lending company. The cash flow and profit and loss budget proves that charging simple interest on all loans, still this lending company can pay dividends, at least equal to the dividend rate paid by National Australia Bank in 2006, just by cutting down, some special payments to CEOs of these entities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}