Westpac Banking Corporation:

(their managers repeated charging only simple interest!)

I complaint to Westpac for charging compound interest and NOT disclosing. Demanded refund the difference.

Rude call from Robyn Clarke of Westpac (she sent letter below, telling to go to ombudsman, not saying anything about compound interest.

Ombudsman replied Page 1, Page 2. He raised his hands up as not aware of their power to deal with this kind of complaint. He wanted to try his luck asking the question to bank.

Minutes of telephone conversation Mr Tim Goss (National resolution manager of Westpac) (on my complaint to ombudsman) , 50 minutes. I asked 5 times if they are charging simple interest or compound interest. He asked me to make a guess of simple or compound!!

He was more of a passive listener (at one point I even thought he went to sleep).

His letter, repeatedly confirmed that they charged ONLY SIMPLE INTEREST on my Loan.

Page 1, Page 2, Page 3, Page 4 Commonwealth Bank of Australia Letter.

False Misleading and deceptive conduct in writing!!!

CEO of CBA knows they are charging only compound interest, but CBA branch managers in Victoria confirm they are charging simple interest.

He confirms as 'industry practice'. This means NO Competition between lenders in relation to compounding monthly, a Section 54 criminal offence under TPA 1974!!!

Ombudsman closed the file with Tim's explanation Page 1, Page 2, Page 3.

Westpac's threat to take over my assets if I did not pay the court cost for my second case before 16th April 2008. Page 1, Page 2, Page 3.

National Australia Bank:

(their managers repeated charging only simple interest!)

Email correspondence Mr Anthony Thompson, (national reconciliation manager of NAB) confirms not aware of charging compound interest.

I complaint to Ombudsman. Ombudsman fixed 18th Dec 06 deadline for NAB to reply. Page 1, Page 2.

No one contacted me from NAB. Mr Alejandro Young's reply, dated 19th Dec 2006 (proving the arrogance not to go by Ombudsman's deadline). Alejandro is a higher level officer than Anthony Thompson. Since Ombudsman system itself is only a 'dispute resolution mechanism' maintained and paid by the Banking industry, how can ombudsman give regulatory instruction?

Mr Young's letter Page 1, Page 2. High handed behaviour threatening me not to go further!

Ombudsman closed the file Page 1, Page 2, Page 3.

Commonwealth Bank of Australia:

(managers assure 100% charging only simple interest!)

Ms Tommy (lending manager of commonwealth bank of Australia, Cheltenham branch)

Mr Gary Carter (manager of Commonwealth Bank of Australia) assured 100% charging only simple interest.

Narelle Hosking & Mario Brex (Commonwealth bank of Australia) not wanting to say compounding.

Justice Marilyn Harbison the head of Anti discrimination wing of VCAT, proves in her judgement she does not know if that was simple interest or compound interest.

I wrote letters encouraging any one of the bank to be the first one to charge Simple interest and get the full market share of borrowers!

Letters sent to CEOs of 14 major lenders in Australia with 'registered post person to person option' (paying additional postage for this special service).

4 CEOs refused to accept delivery of the registered post and sent back (Aussie home loans, Members Equity, Bendigo bank and National Australia bank).

But how did the 4 CEOs knew what was inside registered post?

Have they not proved they have close connections and understandings with other CEOs?) and 4 of the remaining 10 sent replies. Refused AusHL, Refused MEquity, Refused Bendigobank

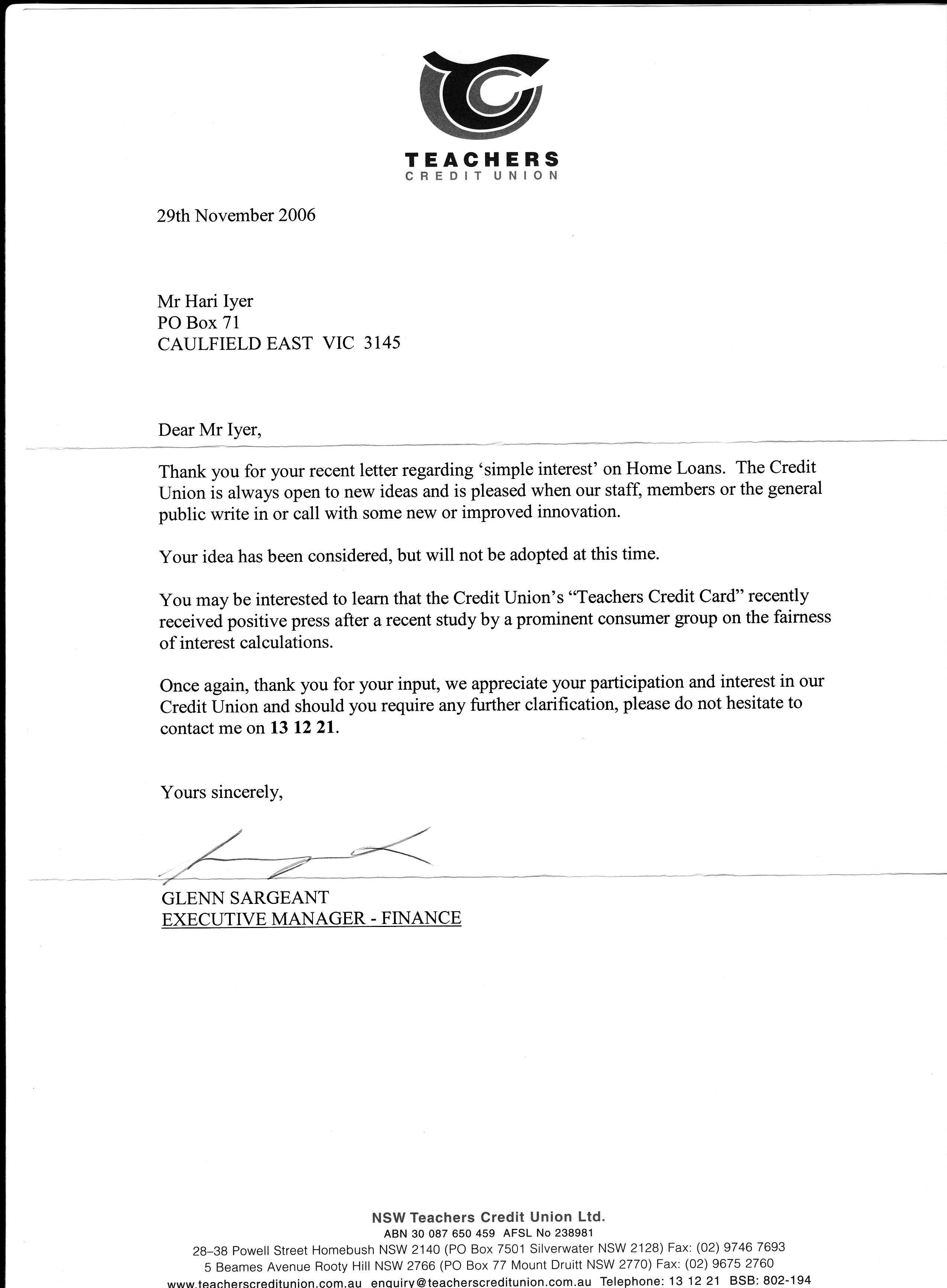

ANZ, Aussie, Bendigo, CBA, credit Suisse, Hsbc, Macquarie, members equity, Mortgage choice, NAB, Rams, StGeorges, Teachers cu, WBC, Wizard.

CBA's reply, St Georg's Reply, Anz's Reply , Teachers credit union reply

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}